Carbon Taxation in 2026: Emissions Trading Scheme (ETS) in expansion.

Carbon pricing trends in 2025 showed a significant expansion in coverage, led by emissions trading schemes (ETS), while direct carbon taxes remained stable.

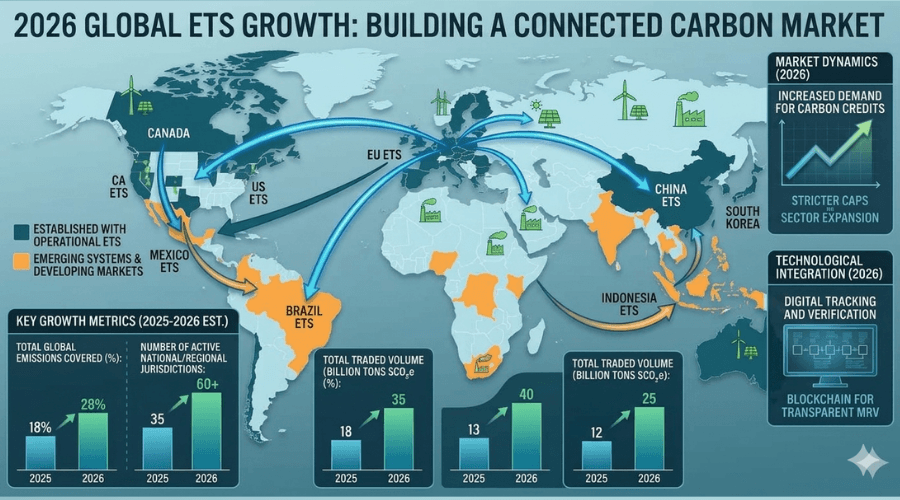

In 2026, approximately 30% of global greenhouse gas (GHG) emissions are covered by some form of carbon pricing mechanism. (CPM).[i]

From April 27 to 30 of this year, the International Conference in Santa Marta (Colombia) will bring together more than 500 Latin American leaders—from government, business, and academia—to accelerate the energy transition by linking carbon pricing mechanisms and taxes with the large-scale deployment of renewables and storage. Its agenda highlights green tax incentives that complement carbon trading schemes, showcases successful models such as Chile’s solar leadership, Brazil’s wind power boom, and Mexico’s green hydrogen initiatives, and explores blended finance that combines multilateral funding with voluntary carbon markets.

These emissions trading schemes raise the cost of fossil fuels, generate funds through auctions that finance renewable energy, implement structural solutions, and reduce baseline emissions, creating a strategic synergy that we analyze below.

1. The surge of Emissions Trading Schemes (ETS)

The main driver of the increase in global coverage by 2025-2026 is the expansion of ETS systems. Coverage under these systems has more than doubled in recent years, reaching approximately 22% of global emissions, and this growth is expected to accelerate.

- • China’s major expansion: A key development in 2025 was the expansion of China’s national emissions trading system to include the aluminum, cement, and steel sectors in March 2025 (retroactively covering 2024 emissions). This single measure significantly increased global coverage to approximately 28% [ii]

- • Sector Expansion: ETS are expanding their presence in key sectors where they are already established and moving into new areas.

- • Electricity and Industry: These sectors remain the primary focus, with more than half of the energy sector’s emissions and approximately 40% of industrial emissions now covered by some form of carbon pricing.

- • Maritime Transport: The EU ETS has been expanded to cover emissions from large cargo and passenger ships, with full coverage expected by 2026. The UK ETS is following a similar path, with the aim of incorporating domestic maritime transport by 2026.[iii]

2. ETS: What Is their Tax Status?

While a carbon tax is a tax-based instrument—where a government sets a price per ton of CO₂ emitted (e.g., $25/t in Colombia)—an ETS is quantity-based: it establishes a total emissions cap and issues tradable allowances; the price is determined by the market (e.g., $45–65/t in the EU ETS for 2026).

Many reports classify ETS as implicit taxes, due to their:

- • Revenue Generation: Auctions generate fiscal revenue (EU ETS: €38.8 billion in 2024, ~63% to Member States).

- • Payment Required: Companies must purchase emission allowances to comply with regulations, much like paying a tax. They also have economic substance: From a fiscal perspective, the ETS imposes a cost on emissions, thereby internalizing externalities.

Others do NOT classify ETS as taxes because:

- • It is a market-based mechanism: the price is determined by supply and demand; it is not fixed. Its legal basis: environmental law (e.g., SEMARNAT in Mexico, MADS in Colombia), not tax law (DIAN)

- • Accounting Standards: Under frameworks such as the IMF’s Government Finance Statistics (GFS), ETS are excluded from the “taxes” category—defined as payments made to the central government without consideration—and are classified as “payments for administrative permits,” since they represent transactions involving acquired rights, not compulsory levies without direct consideration.

Carbon taxes are levies “by design” (tax law), whereas cap-and-trade systems are regulatory frameworks (environmental law) with similar economic effects—internalization of the cost of carbon—whose accounting treatment depends on the legal structure of permits and auctions.[iv]

3. The Stable Role of Carbon Taxes

The established role of carbon taxes remains strong in 2026, covering approximately 5–6% of global GHG emissions, primarily from fossil fuel use in transportation and construction. As of April 2026, 27 countries maintain explicit carbon taxes (27 in 2025), covering roughly 5% of global emissions despite the growth of ETS. They focus on sectors such as aviation and heating.

Various Foundations and Levels

Prices vary widely: <$0.10/tCO₂ (Malaysia), ~$25/tCO₂ (Mexico, Colombia), up to $150+/tCO₂ (Sweden, Uruguay, Switzerland). These differences reflect competing fiscal and climate priorities.

They are integrated within existing policies: Most countries integrate carbon taxes with existing excise taxes (e.g., Colombia via DIAN, Panama), thereby reducing administrative costs. This facilitates subnational expansion (8 states in Mexico by 2026)

4. Emerging Trends and Global Alignment

The year 2025 marked a turning point toward a more integrated and effective global carbon market, a trend that has continued to gain momentum so far in 2026.

- • The Rise of the Carbon Border Adjustment Mechanism (CBAM): The EU’s CBAM, which requires importers to report embedded emissions in products such as steel, aluminum, and cement, has transformed global supply chains and pressured other regions to strengthen their domestic carbon pricing. The United Kingdom launched its own CBAM in January 2026, aligning with the EU and increasing pressure on global exporters.

- • Integration of Offsets: Jurisdictions such as Colombia and Singapore have expanded the use of eligible carbon offsets to meet tax obligations, linking compliance markets with voluntary ones. In 2026, Mexico joined this trend by allowing offsets in its new carbon pricing system, covering 40% of national emissions.

- • Future Growth: Expansion continues with new mechanisms underway in Brazil (a national pilot starting in Q1 2026) and India (an interstate scheme currently being implemented), covering more than 25% of global emissions by the end of the year.

In conclusion, carbon pricing coverage through April 2026 shows steady expansion, driven by emissions trading systems. Although there is not yet a comprehensive global market with high prices, the progress made in 2025–2026 reflects a global commitment to internalizing the cost of emissions, which is key to stabilizing the climate.

We can expect this expansionary trend to accelerate in 2026, beyond specific national markets.

Why Does the Global Trend Persist, in spite of contrary winds?

Several factors ensure the continued growth of this expansion:

- • Subnational momentum in the U.S.: States such as California and those in the Northeast maintain resilient regional markets, with local businesses and governments making progress on decarbonization despite federal policies.

- • Global Market Pressure: The EU and UK CBAMs effectively function as a mechanism for external pressure, pushing exporters to adopt carbon pricing to compete. Otherwise, the EU applies “default values” that are higher and include a 10% surcharge in 2026, which will increase to 30% in 2028, to promote transparency.

- • Corporate and Investor Demand: Thousands of global companies, including U.S. firms, are meeting their net-zero commitments through internal carbon pricing and voluntary markets. The latter exceeded $3 billion in 2025 and is projected to reach $10 billion by 2027, driven by ESG requirements.

In summary, carbon pricing is making solid progress in 2026, with China and Europe strengthening their systems, Mexico and Brazil launching their own, and India stepping up its efforts. The global economy is progressively internalizing the cost of carbon through global taxation.

References:

[i] https://info.calyxglobal.com/webinar-on-demand-the-state-of-quality-and-pricing-in-the-vcm-2026 Regarding the expansion of CO2 emissions coverage.

[ii] International Carbon Action Partnership (ICAP) (2025). “Status Report 2025: Emissions Trading Worldwide – The Sectoral Expansion of China’s National ETS.”

[iii] https://www.gov.uk/government/publications/introduction-of-carbon-border-adjustment-mechanism/carbon-border-adjustment-mechanism

[iv] IMF (2024/2025). “Government Finance Statistics Manual: Treatment of Emissions Trading Permits as Administrative Fees.”

13,603 total views, 110 views today