Meeting of Tax Administrators: Challenges and Opportunities (II) About technology

If we ask the people who lead the tax administrations what makes them lose sleep, they probably won’t answer that it’s some rule of the tax code, or the large number of old debts that are difficult to collect, or even the fact that they are still far from the collection goal.

It is possible, perhaps even probable, that what really keeps them awake at night is the possibility of a cyberattack at two in the morning that manages to affect the tax administration’s services; the news in Monday’s newspaper that the tax return data of politically exposed persons or their relatives has been sold. Or the concern about a systematic abuse of tax refunds, both in the case of exports and benefits associated with a personalized VAT, by malicious actors acting fraudulently, either simulating operations or extorting real beneficiaries; that strikes take place or natural disasters occur that interrupt or paralyze the normal operation of the systems; or even that, under their management and despite their efforts, there are “alternative services” offered in the vicinity of some agency to solve problems in exchange for a negotiable price.

Unfortunately, all of these situations are not just theoretical risks, like a weather forecast for next week that is so frightening that it seems implausible, but rather they have come true as dark prophecies in the past.

And of course, the challenge is to ensure that they never happen again.

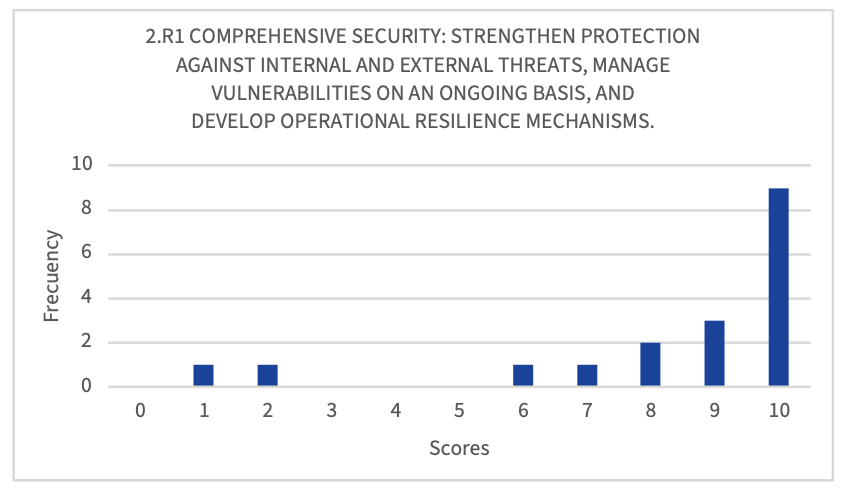

That concern, that challenge does not happen only in the twisted head of this servant. This was confirmed in Montevideo, in October 2025, during a meeting of tax administrators. More than half of the executives identified achieving comprehensive security as the most important challenge in the area of technology, strengthening protection against internal and external threats, continuously managing vulnerabilities, and developing operational resilience mechanisms. This is compounded by the challenge identified in fifth place regarding incident management, with response and continuity plans.

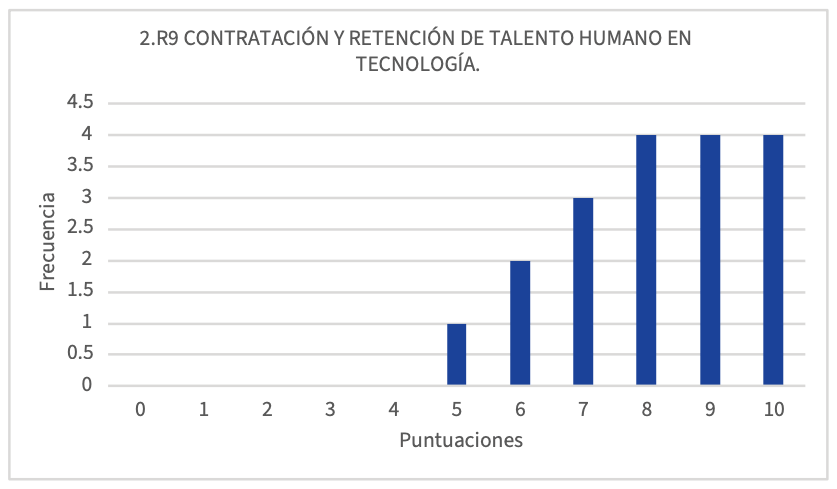

The second most important challenge has to do with the recruitment and retention of human talent in the areas of technology. Alejandro Juárez pointed out to us in previous post that there is a concern about human talent in tax administrations, which is exacerbated in technological areas. We verified that all the administrations present gave a high rating.

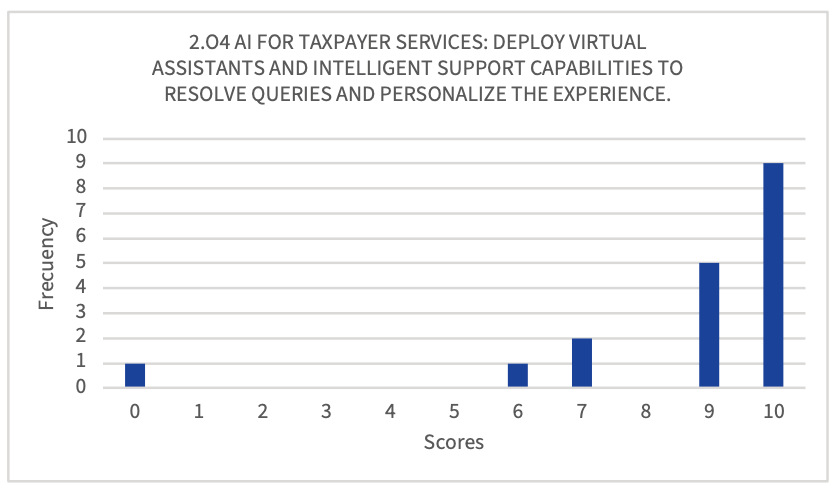

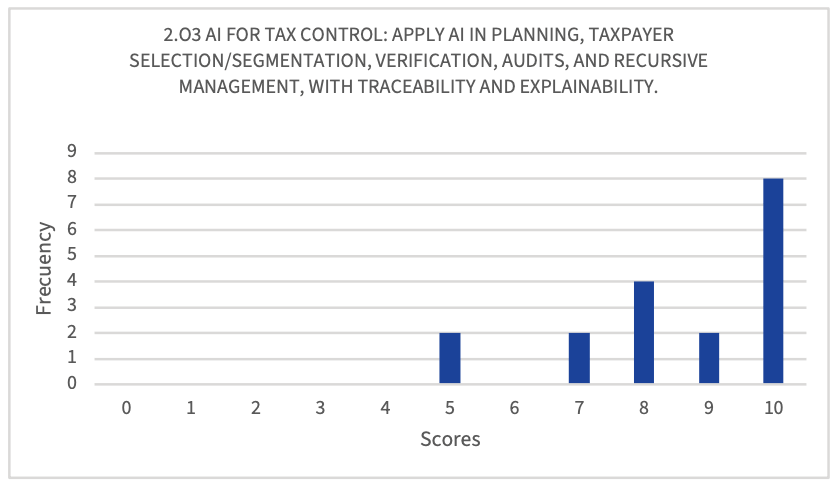

As for the opportunities, the first two come precisely from the use of artificial intelligence in the provision of services, deploying virtual assistants agents with the ability to solve queries and personalize the user experience; and in tax control, applying artificial intelligence in planning, to the selection and segmentation of taxpayers and as support in verification and audit processes as well as in dispute resolution.

At least for now, most tax administrators see in generative artificial intelligence, not our downfall and the end of times, but an opportunity to be more efficient, to do a better job. This support can range from supporting officials to responding to taxpayer inquiries to identifying the arguments and requests raised by the taxpayer in an application or resource so that the case can be assigned rapidly to the most appropriate person or area. In the not-too-distant future, we will even have artificial intelligence agents that help taxpayers properly fulfill all their obligations, avoid mistakes, and prevent penalties.

In the field of tax control, these applications can range from unsupervised mechanisms to identify anomalies and patterns of non-compliance to the identification of evidence of economic substance, or its absence, in transactions with related parties based on the analysis of contractual clauses, internal correspondence and unstructured public information. All this, of course, with care, with safeguards, with good data, and always keeping the official, the human being present.

I should mention that having adequate data governance was rated as both a challenge (fourth in priority) and an opportunity (sixth), perhaps because we find ourselves in a situation that borders on paradox: we have more and more data that must be used with increasing care, in a context that demands the ethical use of artificial intelligence and the need for its explainability.

I also highlight among the opportunities interoperability, compliance by design and automation, which reflect initiatives ranging from pre-filling of declarations to cooperative compliance practices that are advancing in our tax administrations.

The least valued but important aspects, which would otherwise have been left out, were, on the challenging side, the mitigation of risks associated with dependencies on suppliers and service providers; and on the opportunity side, the exploitation, under an appropriate balance—certainly different for each administration—of the combination of internal capabilities and outsourced services.

In the document about the Meeting, published by the Secretariat last January, you can consult in detail the averages and their standard deviations, of all the eleven challenges and eleven opportunities, as they were identified and assessed at the Montevideo conference. Go ahead, download it and study it… here is the link

Greetings and Godspeed.

2,153 total views, 8 views today