Global Inventory 2025 – Where Are Tax Administrations Now, and Where Are They Headed in Terms of Digitalization and Digital Transformation? Part 3

1) Introduction

In this third installment of the [i] series (Part 3), we continue addressing the question: where do tax administrations currently stand, and where are they heading in terms of digitalization and digital transformation?

On this occasion, the analysis focuses on taxpayer touchpoints, understood as the set of channels, interfaces, and mechanisms through which taxpayers access information, fulfill their obligations, and interact digitally with the tax authority. [ii] This is a particularly crucial area, as it represents the exact space where digitalization transcends mere institutional architecture and transforms into a real-world compliance experience.

Given that this pillar of Tax Administration 3.0 encompasses multiple dimensions, this analysis focuses on four particularly relevant capabilities to assess the degree of digitalization of tax compliance globally and, in greater detail, in Latin America and the Caribbean (LAC): 1) Online tax registration, 2) Online tax filing, 3) Online tax payments, and 4) Payments processed instantly and reflected in account balances.

The selection of these capabilities is based on a fundamental rationale. Together, they allow us to observe the transition from the availability of essential online services—capabilities 1), 2), and 3)-to more advanced forms of automated response—capability 4). In other words, they allow us to assess not only whether taxpayers can comply digitally, but also whether the tax administration has begun to reduce operational friction through immediate system responses. . [iii]

2) Development

As previously noted, capabilities 1), 2), 3), and 4) provide a highly concrete demonstration of how digitalization translates into effective compliance practices. This is precisely where the taxpayer registers, files returns, makes payments, and interacts digitally with the tax authority. To offer a clearer comparative analysis, Table 1 summarizes the regional evidence for 13 Latin American and the Caribbean (LAC) countries [iv] by capability and tax type—Personal Income Tax (PIT), Corporate Income Tax (CIT), and Value Added Tax (VAT)—while Table 2 presents the country-by-country coverage across the four analyzed capabilities. Capabilities 1), 2), and 3) illustrate the extent of essential online services, whereas capability 4) identifies a more demanding standard linked to automated responses within a digital environment.

2.1) Essential online services in the global context and in Latin America and the Caribbean

The global report shows that, in a growing number of jurisdictions, the modernization of taxpayer touchpoints is no longer limited to moving traditional procedures to the digital environment but is moving toward more integrated and taxpayer-centered interaction models. [v] Within this landscape, three of the most representative services of basic digital compliance are: 1) online tax registration, 2) online tax filing, and 3) online tax payments.

On a global scale, capability 2) Online tax filing achieves near-universal implementation across the three main tax types considered—PIT, CIT, and VAT—with percentages of 100%, 98.1%, and 100%, respectively. Similarly, capability 1) Online tax registration and capability 3) Online tax payments also display a very high level of implementation, falling within approximate ranges of 87% to 92%, depending on the type of tax. [vi] Taken together, these results suggest that, on a global level, the core engine of tax compliance is already extensively digitalized.

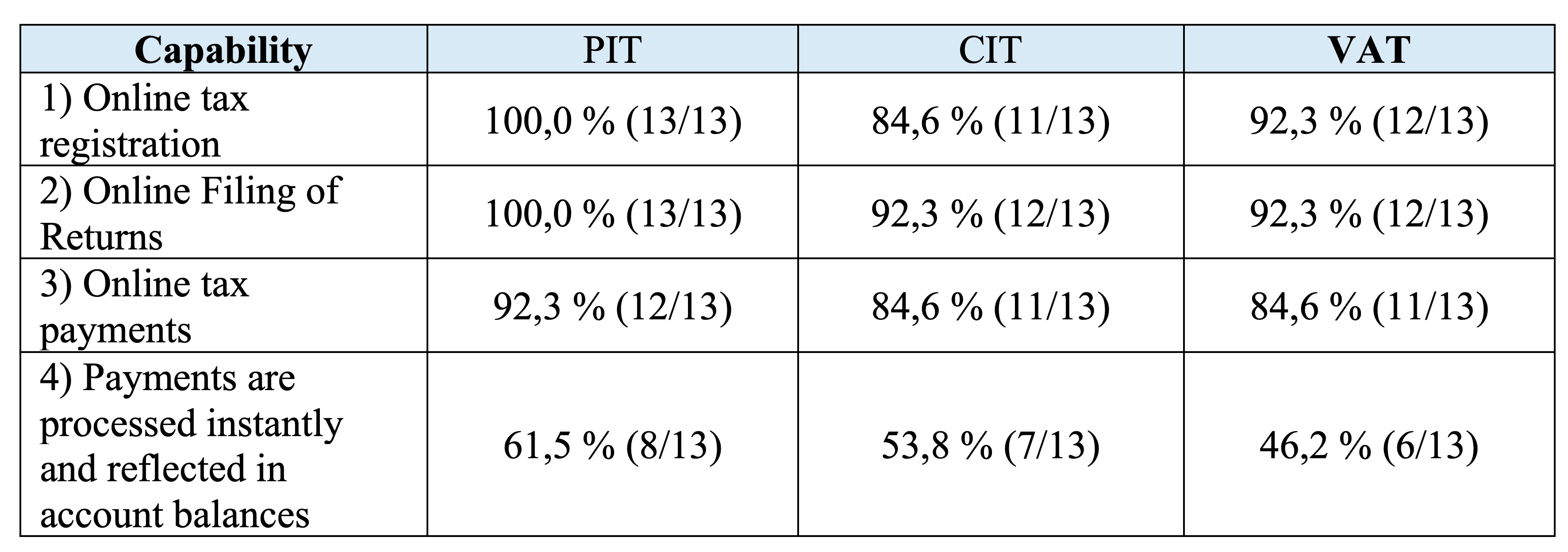

Regional data from Latin America and the Caribbean (LAC) show a similar pattern. In fact, capability 1) Online tax registration reaches 100% for personal income tax (PIT), 84.6% for corporate income tax (CIT), and 92.3% for VAT. Capability 2) Online filing of returns shows similarly high levels: 100%, 92.3%, and 92.3%, respectively. Meanwhile, capability 3) Online tax payments also shows significant coverage, at 92.3% for personal income tax and 84.6% for both corporate income tax and VAT. . [vii] (see Table 1 below).

Table 1. Percentage of LAC countries reporting the four key functions of taxpayer contact points, by type of tax

Source: Compiled by the author based on the Inventory of Tax Technology Initiatives, available as of April 15, 2026 (OECD Data Explorer). Note: Percentages calculated based on the total of 13 LAC countries. The numbers in parentheses indicate the number of countries that reported “Yes” for each capability.

As can be seen, the three basic functions of digital compliance—online registration, filing, and payment—are widely adopted in the region. However, function 4), which involves the instant processing of payments and their reflection in balances visible to the taxpayer, shows more moderate levels of adoption.

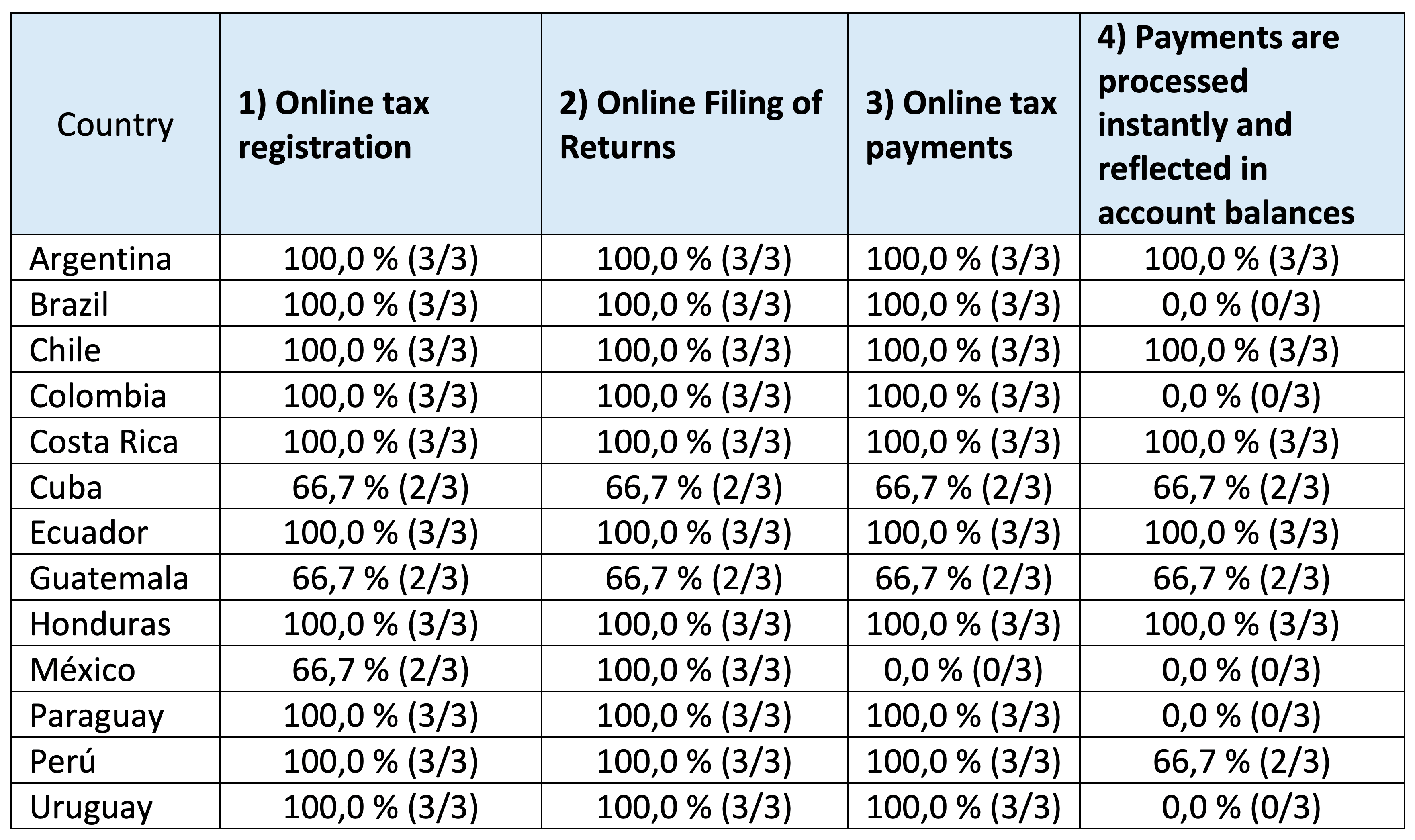

See Table 2 below, which presents data disaggregated by country, based on the observations available for each function (1), (2), (3), and (4) and type of tax—personal income tax, corporate income tax, and VAT—[viii]. This approach makes it possible to identify not only the aggregate regional level but also the intensity of the reported deployment in each jurisdiction

Table 2. Percentage of coverage by country for four key functions of taxpayer contact points in Latin America and the Caribbean

Source: Own elaboration based on the Inventory of Tax Technology Initiatives, available as of April 15, 2026 (OECD Data Explorer).

Note: Each percentage is calculated based on 3 possible observations per capability and country (PIT, CIT, and VAT). For a combined analysis of capabilities 1), 2), and 3), 9 possible observations per country can be aggregated.

Countries with unreported observations for capabilities 1), 2), and 3): Cuba (VAT) and Guatemala (CIT).Countries with unreported observations for capability 4): Cuba (VAT), Guatemala (CIT), Mexico (PIT, CIT, and VAT), and Paraguay (PIT, CIT, and VAT).The absence of affirmative responses does not necessarily equate to the material absence of the capability. Consequently, the percentages must be interpreted as levels of self-reported deployment within the ITTI, rather than an external verification of the material existence or non-existence of each capability.

Based on the disaggregated data in Table 2, a second analysis can be conducted, this time by country, using the nine possible combinations resulting from the intersection of capabilities 1), 2), and 3) with the three types of taxes considered—personal income tax (PIT), corporate income tax (CIT), and value-added tax (VAT)—as a reference. From this perspective, the regional landscape of Latin America and the Caribbean reveals a particularly broad digital base:

- High levels (81 % to 100 %): Argentina, Brazil, Chile, Colombia, Costa Rica, Ecuador, Honduras, Paraguay, Peru, and Uruguay.

- Intermediate levels (61 % to 80 %): Cuba and Guatemala, both with 66,7 %.

- Low levels (41 % to 60 %): México, with 55,6 %.

A comparative analysis thus shows that, in Latin America and the Caribbean, the digitalization of functions 1), 2), and 3) is well established across a significant portion of the region. In most of the countries analyzed, online registration, filing, and payment are already part of the basic institutional framework. At the same time, Table 2 reveals that this coverage is not entirely uniform, as there are still cases where the reported implementation is partial or contains reporting gaps.

2.2) A higher level of digitalization: payments processed instantly and reflected in the taxpayer’s checking account balance

It is important to note that the mere existence of basic digital services does not exhaust the analysis. It is one thing for a taxpayer to be able to file a return and make a payment online, but it is quite another for that payment to be processed instantly and automatically reflected in their visible account balances. This second dimension represents a more demanding standard, as it introduces a clear element of operational automation on the part of the tax administration.

On a global scale, the report shows that capability 4) Payments processed instantly and reflected in account balances still displays more moderate implementation levels than those observed for essential online services. The instant processing of payments and their automatic reflection in balances visible to the taxpayer stands at around 46.2% for personal income tax, and slightly above 50% for both corporate income tax and VAT[xi]. This suggests that while the digitalization of tax payments is already widespread, the full automation of this interaction has not yet achieved the same level of diffusion.

In LAC, the pattern is similar. Capacity 4) Payments processed instantly and reflected in account balances stands at 61.5% for personal income tax, 53.8% for corporate income tax, and 46.2% for VAT. This evidence suggests that a significant portion of the region’s tax administrations has already moved beyond merely enabling digital payments toward more streamlined forms of automated processing, although this progress remains clearly less widespread than that observed for capabilities 1), 2), and 3) considered in isolation (see Table 1).

Also, regarding this aspect of capacity 4), Table 2 allows for a comparative analysis by country, based on the three possible observations corresponding to the three types of tax—personal income tax, corporate income tax, and VAT. From this perspective, the regional picture is more uneven:

- High levels (81 % to 100 %): Argentina, Chile, Costa Rica, Ecuador, and Honduras (100%).

- Intermediate levels (61 % to 80 %): Cuba, Guatemala (66.7%), and Peru (66.7%),

- No affirmative responses reported in this section (0%): Brazil, Colombia, Mexico, Paraguay, and Uruguay. [x]

This breakdown clearly shows that the gap between available digital services and effective automated responses remains one of the most striking features of the digital transformation process in tax administrations across Latin America and the Caribbean. In other words, a significant number of government agencies have already made features 1), 2), and 3) available to taxpayers in a digital environment; however, a smaller proportion has moved toward interactions in which the system automatically processes the payment and updates the taxpayer’s status in real time, for example, in their tax checking account.

Taken as a whole, Table 2 reveals a particularly telling contrast: several countries that report full coverage for functions 1), 2), and 3) do not, however, report the same level of implementation for capacity 4). This reinforces the idea that digitalizing a process does not necessarily mean automating the response. It is precisely in this transition that a key analytical distinction begins to emerge, one that is essential for understanding the current state of digital transformation in tax administrations across Latin America and the Caribbean.

3) Conclusions

Three main points can be highlighted from the above. First, Latin America and the Caribbean have made significant progress in the digitalization of basic tax compliance services. Online registration, filing, and payments have seen high levels of adoption, generally in line with the global landscape.

Second, the evidence shows that digitalization is not progressing at the same pace across all functions. While basic services have broad coverage, the instant processing of payments and their reflection in balances visible to taxpayers show more moderate levels and significant differences between countries.

Finally, the comparison shows that having digital services does not necessarily mean having fully automated interactions. ALC has established a solid foundation for digital tax compliance, but the next challenge is to further integrate and automate these services in order to move toward a simpler, more immediate, and smoother compliance experience

4) Next installment (Part 4)

The next installment will focus on pillar (3), “Data Management and Standards,” to examine how tax administrations in Latin America and the Caribbean are strengthening their capabilities in data collection, standardization, interoperability, and strategic use of data, as well as their degree of alignment with the principles of Tax Administration 3.0.

References:

[[i]] See Parts 1 and 2 of the series below: Part 1: https://www.ciat.org/inventario-global-2025-donde-estan-y-hacia-donde-van-las-administraciones-tributarias-en-el-ambito-de-la-digitalizacion-y-transformacion-digital-parte-1/ and part 2: https://www.ciat.org/inventario-global-2025-donde-estan-y-hacia-donde-van-las-administraciones-tributarias-en-el-ambito-de-la-digitalizacion-y-transformacion-digital-parte-2/

[[ii]] OECD (2025), Tax Administration Digitalization and Digital Transformation Initiatives, OECD Publishing, Paris, https://doi.org/10.1787/c076d776-en. Página 20. (Consulted on May 9, 2026).

[[iii]] It is worth noting in this Part 3 that the “Inventory of Tax Technology Initiatives” is compiled from information gathered through the “Global Survey on Digitalization” and is structured around the six pillars of the “Tax Administration 3.0” approach. Since this information is provided by the tax administrations themselves, the data should be considered self-reported, as it has not been reviewed or validated by the OECD or its partner organizations.

[[iv]]This Part 3 continues the analysis of the 13 Latin American and Caribbean countries selected in accordance with the methodology outlined in Part 2: 1) Argentina, 2) Brazil, 3) Chile, 4) Colombia, 5) Costa Rica, 6) Cuba, 7) Ecuador, 8) Guatemala, 9) Honduras, 10) México, 11) Paraguay, 12) Perú y 13) Uruguay.[[v]]OECD (2025), Tax Administration Digitalization and Digital Transformation Initiatives, OECD Publishing, Paris, https://doi.org/10.1787/c076d776-en. (Consulted on May 09, 2026).

[[vi]] Tax Administration Digitalization and Digital Transformation Initiatives, OECD Publishing, Paris, https://doi.org/10.1787/c076d776-en Page 21, Table 3.1. Online services offered by tax administrations by tax type, 2024 (Consulted on May 09, 2026).

[[vii]] Inventory of Tax Technology Initiatives available as of October 1, 2025, on the OECD Data Explorer (Consulted on April 15, 2026).https://data-explorer.oecd.org/vis?tm=inventory%20of%20tax&pg=0&snb=80&df[ds]=dsDisseminateFinalDMZ&df[id]=DSD_QDD_ITTI%40DF_QDD_ITTI&df[ag]=OECD.CTP.TAV&dq=.&to[TIME]=false

[[viii]]Tax Administration Digitalization and Digital Transformation Initiatives, OECD Publishing, Paris, https://doi.org/10.1787/c076d776-en Page 22, Table 3.3. Online services offered by tax administrations by tax type, 2024 (Consulted on May 09, 2026).

[[ix]]In several cases within sub-block 4 of the capability, there are observations that were not reported; therefore, the absence of affirmative responses should not automatically be interpreted as a material absence of the capability. Even so, the comparative pattern shown in the tables does indicate that the transition from the digitization of the process to the automation of the response remains uneven across the region

2,999 total views, 71 views today