The Recalcitrant Tax Debtor: Assessment and Measures

The tax debt: its normalization

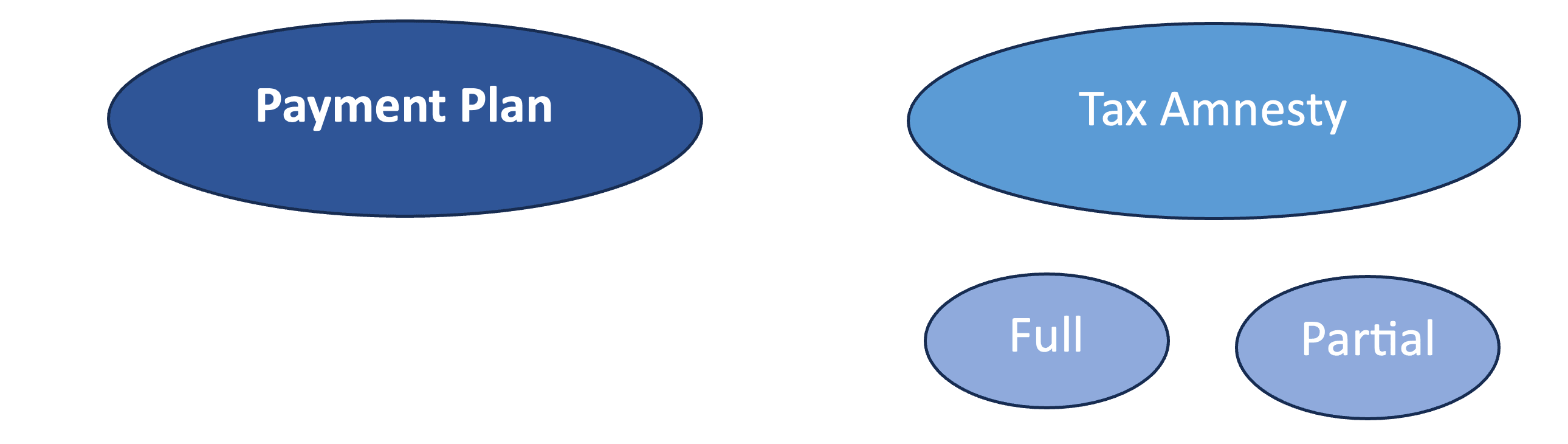

Taxpayers through their tax history may have periods of financial crises, which prevent them from paying taxes on time and in a timely manner. For this reason, countries have various payment contingency plans in order to regularize their situation[1].

When some kind of pardon is granted, the so-called “tax amnesties” arise, which are classified into full and partial ones. The first ones involve the capital, interests, and the sanctions, while the partial ones only comprise the interest, fines, and penalties.

The full ones can be in turn: gratuitous or onerous. The first are exceptional; in the latter, tax debts are usually regularized by paying an extraordinary tax with a special taxable base and aliquot, which is determined for each occasion.

SETTLEMENT OF TAX OBLIGATIONS

It has been proven that repeated tax amnesties undermine tax compliance, since a significant portion of delinquent taxpayers—rather than paying on time (even when they have the financial means to do so)— focus their expectations on settling their obligations during the next amnesty in order to benefit from their advantages[2].

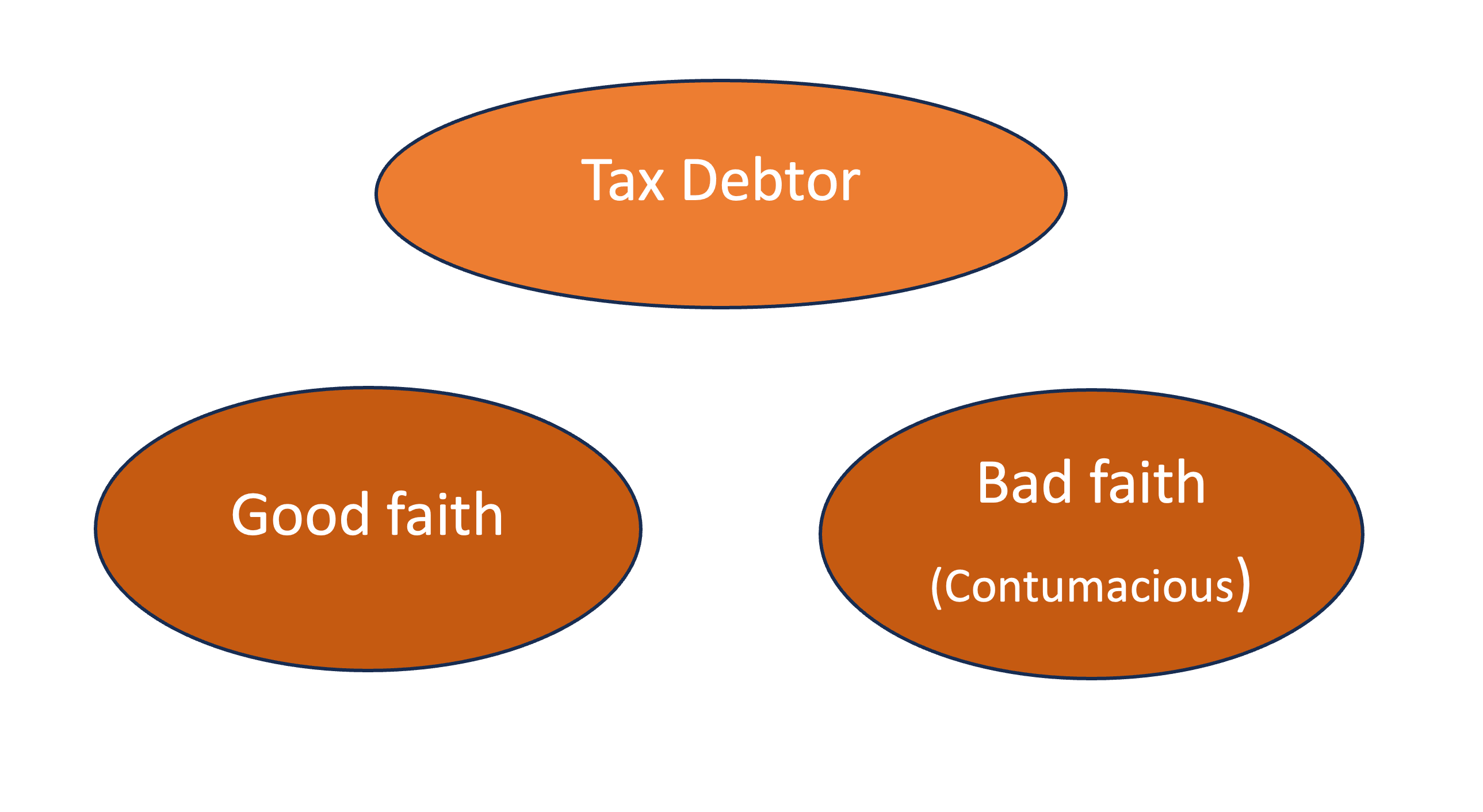

Types of debtor

In this universe, there are two clearly differentiated categories of debtors[3]:

- Those acting in good faith: that is, those who, due to general or individual economic situations, are temporarily unable to comply with their tax obligations on time.

- those acting in bad faith[4]: their goal and business strategy is to avoid paying taxes in order to increase their profitability and gain an unfair economic advantage over their competitors by reducing their costs.

Strategies

Is it valid to apply the same strategy in the normalization of debts without considering the class of debtor?

As there are different classes of debtors, a “laissez-faire” policy can be applied[5] or on the contrary, an active policy, that is, to adopt measures within the administrative or judicial sphere differentiated according to whether the debtors acted in good or bad faith.

In Latin America, most countries have adopted a “laissez-faire” approach, failing to implement differentiated policies for this category of debtors, thereby allowing unfair practices to persist and spread. These practices not only distort competition in the market but also clearly harm the public treasury.

The Brazilian case: The Contumacious tax debtor

Through its Complementary Law No. 225 of 2026, Brazil has introduced in its legislation the legal concept of the “recalcitrant tax debtor”, defining it as the taxpayer whose behavior is characterized by substantial, reiterated[6] and unjustified[7] non-payment of taxes[8].

For a tax debt to be considered substantial, as far as federal taxes are concerned, the total debt must be equal to or greater than R$ 15 million (USD 2.8 million) and equivalent to more than 100% of the debtor’s known assets.

This also applies to taxpayers who are related parties (such as a parent company or subsidiary) of a company that has been declared ineligible or that has closed in the last five years with tax debts of R$ 15 million or more (approx. USD 2.8 million).

The procedure designating this debtor begins when the Receita Federal identifies a possible candidate, to whom it notifies and grants a period of 30 days for the payment of the debt or the presentation of its defense (with suspensive effect).

The business confederations can formulate objections to the classification of their member companies, until the final administrative decision, but without legitimation to appeal the decision.

However, in some situations the process is not suspended, for example: a) when the company was created to commit fraud or tax evasion, b) if the company has participated, according to evidence, in an organization formed to avoid paying taxes, and c) when using stolen, counterfeit, adulterated or smuggled products

Taxpayers who are administratively sanctioned as recalcitrant debtors are barred from receiving any type of tax benefit, including using tax losses to offset taxes. They are also precluded from participating in public tenders or requesting Insolvency protections.

Furthermore, their CNPJ (Tax Identification Certificate) is suspended and at the federal level, they will be subject to administrative procedures with fewer options to file legal challenges.

The Receita Federal must include these debtors in a registry. To this end, the tax authorities of other federal entities must report the inclusion and exclusion of taxpayers in this category. The process is closed if the debtor pays the debt in full, or it is suspended if he negotiates a payment plan and remains current. However, if the debtor deliberately delay payments, the tax administration may revoke its decision and re-consider the taxpayer as a contumacious debtor.

The investigated taxpayer will cease to be characterized in this category when he proves the existence of assets of equal or greater value than his debts and has not generated new defaults.

To assess the negative economic impact of this class of taxpayers, in 2025 the Receita Federal estimated that only 1,200 recalcitrant debtors owed approximately R$ 250 billion (USD 46 billions) to the public treasury.

Conversely, this strategy includes incentives for taxpayers with a good payment record, such as:

- a) Access to simplified care channels for orientation and regularization,

- b) Flexible of the rules for acceptance or replacement of guarantees,

- c) Deferring the execution of guarantees in tax execution procedures until after the final judgment of the related litigation.

- d) Priority in the analysis of administrative processes, especially those involving tax credits.

Summary:

The classic strategy of treating all tax debt, regardless of the tax debtor behavior, has not yielded encouraging results in debt collection in developing countries. As Albert Einstein famously said: “If you are looking for different results, do not always do the same thing”.

Therefore, the initiative—which provides incentives for timely taxpayers and imposes restrictive measures on persistent defaulters—represents an appropriate strategy in the region’s current context. It improves voluntary compliance with tax obligations by preventing abuses by bad-faith debtors.

Given that tax regulations vary by country, the classification of a recalcitrant taxpayer, the procedure for determining such status, the restrictive measures applied as a result, and the resulting restrictive measures must be evaluated by each specific jurisdiction.

References:

[1] These are known as payment plans, installment plans, etc. The interest rate applied is a key factor in determining them, as it is lower than the statutory interest rate. For their configuration, countries consider the size of the taxpayer, the amount of the debt, the existence of guarantees, etc.

[2] Weighing the profits they would make by investing that capital in their business or the financial market, or by paying the tax on time, against the benefit they gain by joining the settlement plan.

[3] “The recalcitrant tax debtor,” CIATBlog

[4] They may or may not be habitual. This clarification responds to the criterion that identifies habituality as the only element to be considered to determine good or bad faith.

[5] No policy is adopted to restrict or modify what happens, regardless of the possible negative consequences that it may cause.

[6] The existence of tax credits in an irregular situation for at least 4 (four) consecutive assessment periods, or for 6 (six) alternate assessment periods, in a 12 (twelve) month period.

[7] The absence of objective reasons for the non-payment. If a moratorium has not been granted, nor the full amount has been deposited or an adequate guarantee has been provided, a payment plan has been established, nor a court order has been issued suspending the enforceability of the tax liability.

[8] The lack of known assets in an amount equal to or greater than the principal of the debt.

3,519 total views, 11 views today